By Neo | Finaa

Personal finance writer focused on practical budgeting strategies for beginners. I’ve spent years testing simple money systems to help people take control of their finances without feeling restricted.

You get paid… and a few weeks later, your bank account is almost empty.

No big purchases. No clear reason. Just bills, small expenses—and somehow, your money is gone.

If this sounds familiar, you’re not alone. Most people don’t struggle because they earn too little—they struggle because they don’t have a clear plan for their money.

That’s exactly what a monthly budget solves.

A good budget doesn’t restrict your life—it gives you control. It helps you spend without guilt, save with purpose, and finally understand where your money is going.

In this guide, you’ll learn how to create a monthly budget step-by-step, even if you’ve never done it before.

What Is a Monthly Budget?

A monthly budget is a simple plan that shows:

- How much money you earn

- How much you spend

- Where your money goes

- How much you save

Think of it like a GPS for your finances. Without it, you’re guessing. With it, you’re making intentional decisions.

Why Most Budgets Fail (And How to Avoid It)

Let’s be honest—most people try budgeting and quit within a month.

Not because budgeting is hard… but because they make these mistakes:

- They make their budget too strict

- They forget real-life expenses

- They don’t track spending

- They expect perfection

👉 Here’s the truth:

Budgeting isn’t about being perfect—it’s about being consistent.

Step-by-Step Guide to Creating a Monthly Budget

Step 1: Calculate Your Monthly Income

Start with your total monthly income (after taxes).

Include:

- Salary or wages

- Freelance or side income

- Business income

- Any consistent income sources

Example:

- Job income: $3,200

- Side income: $400

- Total income: $3,600

👉 If your income varies, use your average from the last 3–6 months.

Step 2: List All Your Expenses

Now write down everything you spend money on.

Fixed Expenses (Same Every Month)

- Rent: $1,200

- Car payment: $300

- Insurance: $150

- Subscriptions: $50

Variable Expenses (Change Monthly)

- Groceries: $400

- Transportation: $180

- Dining out: $250

- Entertainment: $120

👉 Small expenses matter more than you think—they quietly drain your budget.

Step 3: Track Your Spending (Don’t Skip This)

This is where most people go wrong.

You think you know your spending—but the numbers often tell a different story.

Track your spending for at least 30 days using:

- A notes app

- A spreadsheet

- A budgeting app

Real example:

You think you spend $100 eating out…

But tracking shows it’s actually $280.

That $180 difference? That’s your opportunity to save.

Step 4: Compare Income vs. Expenses

Now do the math:

- Income: $3,600

- Expenses: $2,900

- Remaining: $700

This leftover money is your power.

You can use it to:

- Save

- Invest

- Pay off debt

👉 If your expenses are higher than your income, don’t panic—that’s exactly why you’re budgeting.

Step 5: Set Clear Financial Goals

A budget without goals doesn’t work.

Ask yourself:

- Do I want to build an emergency fund?

- Pay off debt?

- Save for something important?

Simple goal examples:

- Save $1,000 in 3 months

- Pay off $2,000 debt

- Build a starter emergency fund

👉 Your goals give your money direction.

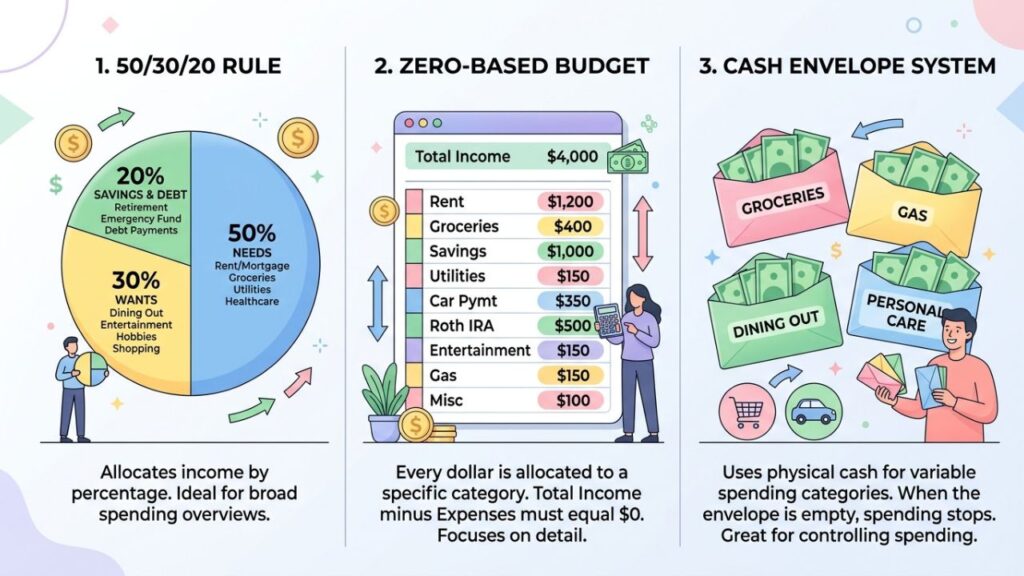

Step 6: Choose a Budgeting Method

Pick a system that fits your lifestyle:

1. 50/30/20 Rule

- 50% → Needs

- 30% → Wants

- 20% → Savings/Debt

2. Zero-Based Budget

Every dollar has a job.

Income – Expenses = 0

3. Envelope Method

Use cash for categories. When it’s gone—you stop spending.

👉 For beginners, the 50/30/20 rule is the easiest starting point.

Step 7: Adjust Your Spending

If your numbers don’t work, make small changes.

Look for easy wins:

- Reduce eating out

- Cancel unused subscriptions

- Compare grocery prices

- Limit impulse buying

Example:

- Dining out: $250 → $150

- Shopping: $150 → $80

👉 That’s $170 saved instantly.

Step 8: Build an Emergency Fund

Life happens—unexpected expenses are part of reality.

Start small:

- First goal: $500–$1,000

- Long-term: 3–6 months of expenses

Even saving $50–$100/month builds real security over time.

Step 9: Review Your Budget Monthly

Your budget isn’t a one-time task.

At the end of each month:

- Review what you spent

- Compare it to your plan

- Adjust for next month

👉 Your budget should evolve with your life.

Real-Life Example: Simple Monthly Budget

Income: $3,000

Expenses:

- Rent: $1,000

- Utilities: $200

- Groceries: $350

- Transportation: $150

- Insurance: $150

- Dining out: $150

- Entertainment: $100

Savings & Debt:

- Emergency fund: $300

- Debt: $200

Total: $2,600

Remaining: $400

👉 This extra money can act as a buffer or boost savings.

What I Learned After Sticking to a Budget

When I first started budgeting, I made a simple mistake—I tried to cut everything at once.

It didn’t work.

What actually worked was:

- Making small adjustments instead of drastic cuts

- Tracking spending weekly (not just monthly)

- Leaving room for enjoyment

👉 The biggest lesson:

A budget only works if it’s realistic enough to stick to.

Tips for Sticking to Your Budget

- Start simple—don’t overcomplicate

- Be realistic—don’t cut everything you enjoy

- Automate savings

- Check your budget weekly

- Adjust when needed

👉 Consistency beats perfection every time.

Common Mistakes to Avoid

- Being too strict

- Ignoring small expenses

- Not tracking spending

- Forgetting irregular costs

- Giving up too early

👉 Budgeting is a skill—you improve with time.

Frequent Q&A

1. What if I live paycheck to paycheck?

Start by tracking expenses and cutting small costs. Even saving a small amount matters.

2. Should I use an app or spreadsheet?

Use whatever you’ll actually stick with.

3. How much should I save monthly?

Aim for 10–20%, but start small if needed.

4. What if my income changes?

Use your average income and adjust monthly.

5. How long before I see results?

Most people notice improvements within 2–3 months.

Conclusion

Creating a monthly budget might feel overwhelming at first—but it’s one of the most powerful steps you can take for your financial future.

A simple budget helps you:

- Take control of your money

- Reduce stress

- Build savings

- Reach your goals faster

Start small. Stay consistent. Adjust as you go.

You don’t need a perfect budget—you just need one that works.